Capital Markets: Commission fans headwinds (NZ Herald)

“The findings of the Australian Royal Commission have been far more material than anticipated,’ say UBS in a research report out this month.

Christopher Simcock, Country Head, UBS New Zealand, says the Australian banks are looking to divest or get back to their core business.

“The regulators have made it very clear they’re not prepared to tolerate any bad behaviour,” says Simcock. “And we’ve seen through many, many cycles, that these huge organisations, these huge conglomerates, are very difficult to control.

You might have the best systems in the world but if you’ve got 150,000 employees doing 57 different things in 74 different countries, it’s tough being a board member presiding over that.

“Whereas if you’ve got that number of staff in that many countries doing three things you’ll probably sleep better in the evenings.”

Executive Director of Investment Banking Andrew Fredericks points to UBS analysis suggesting one risk is the Royal Commission being a catalyst for a credit crash in Australia.

“When you look at some of the work done in that sector on interest only loans, those changes got made a year ago, we think it’s 2019, 2020 when that bow-wave really hits the consumption side, when people have to move to principal as well as interest only,” he says.

The concern in Australia is that the response by banks to apply more stringent standards in respect of customers’ income, expenses, assets and liabilities could lead to a sharp reduction in credit availability. This could have implications on house prices, consumption and growth.

Despite claims that New Zealand banks operate under a different regulatory and governance framework, there are concerns these same implications could spill over to New Zealand’s Australian-owned banks.

This concern prompted the FMA and RBNZ to meet with the chief executives of New Zealand’s registered banks. Earlier this month they issued an open letter to banks requiring written responses by May 18 that detail what actions have been taken to mitigate the risk of misconduct.

The letter says: “We expect you to show us what you have done in order to be comfortable that there are no material conduct issues within your business. We anticipate that you will have undertaken an exercise of that nature after our Conduct Guide and may be extending or enhancing that work in response to issues raised at the Royal Commission or more broadly as a result of that inquiry.”

“I don’t know how the banks are going to respond to that letter from the FMA and RBNZ, but they were given three weeks to do it, and I would have thought they are going to be very cautious on credit availability,” says Fredericks.

David Lane, UBS’s Head of NZ Equities says executives and boards of local banks have been quite careful.

“They started putting in place — probably prior to the macroprudential requirements — cleaning up their balance sheets. We haven’t seen the banks take any major hits on construction or apartment buildings — it’s been the promoters that have worn it. Having the pre-sale requirements and the bonds, etc, the banks have been quite careful.”

The research report from UBS says: “It is impossible to be definitive about the possible flow-on effects from the Australian Royal Commission to New Zealand, other than to say, from an economic perspective, they can only be negative risks. Moreover, the greater the fallout in Australia, the greater the downside risks (direct and indirect) will be for New Zealand.”

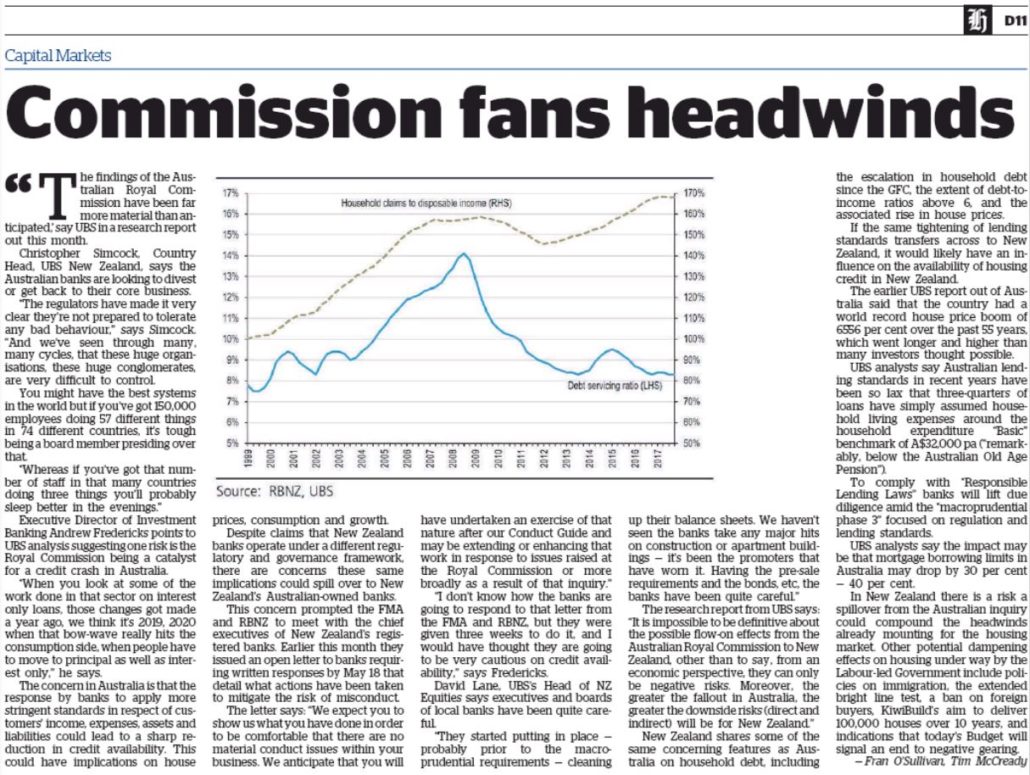

New Zealand shares some of the same concerning features as Australia on household debt, including the escalation in household debt since the GFC, the extent of debt-to-income ratios above 6, and the associated rise in house prices.

If the same tightening of lending standards transfers across to New Zealand, it would likely have an influence on the availability of housing credit in New Zealand.

The earlier UBS report out of Australia said that the country had a world record house price boom of 6556 per cent over the past 55 years, which went longer and higher than many investors thought possible.

UBS analysts say Australian lending standards in recent years have been so lax that three-quarters of loans have simply assumed household living expenses around the household expenditure “Basic” benchmark of A$32,000 pa (“remarkably, below the Australian Old Age Pension”).

To comply with “Responsible Lending Laws” banks will lift due diligence amid the “macroprudential phase 3” focused on regulation and lending standards.

UBS analysts say the impact may be that mortgage borrowing limits in Australia may drop by 30 per cent — 40 per cent.

In New Zealand there is a risk a spillover from the Australian inquiry could compound the headwinds already mounting for the housing market. Other potential dampening effects on housing under way by the Labour-led Government include policies on immigration, the extended bright line test, a ban on foreign buyers, KiwiBuild’s aim to deliver 100,000 houses over 10 years, and indications that today’s Budget will signal an end to negative gearing.

Leave a Reply

Want to join the discussion?Feel free to contribute!