Dynamic Business: A ‘Kodak’ moment for banks (NZ Herald)

If the companies within the financial services industry are to survive the fourth industrial revolution, they must embrace emerging technologies.

That was the message from Likhit Wagle, IBM Asia Pacific’s general manager financial services, at the 2018 INFINZ conference this month.

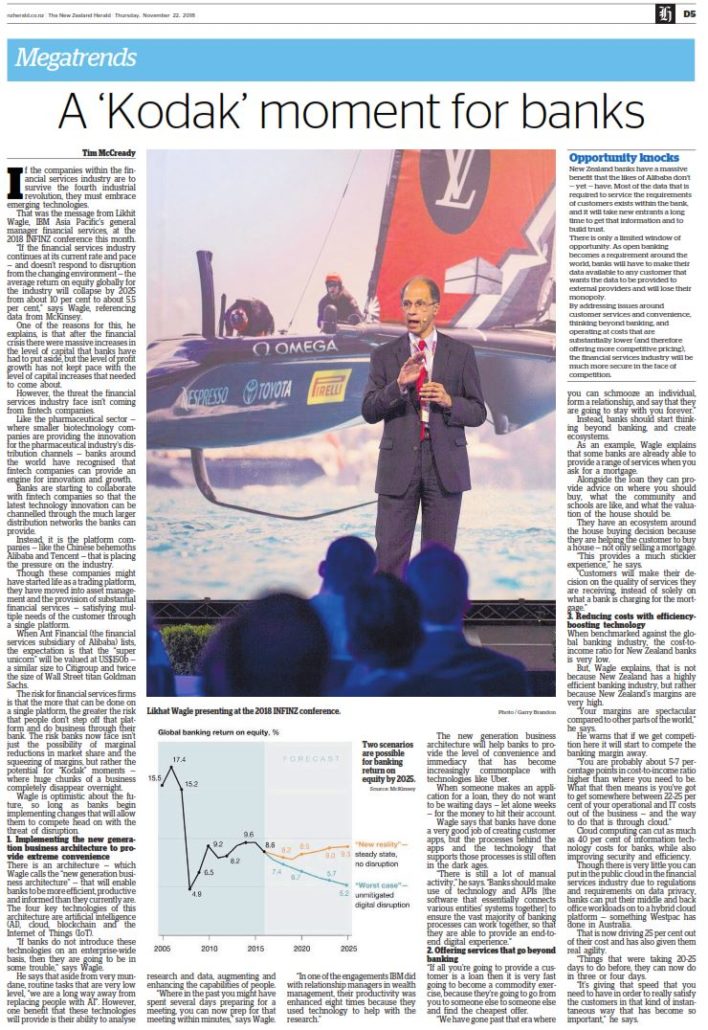

“If the financial services industry continues at its current rate and pace — and doesn’t respond to disruption from the changing environment — the average return on equity globally for the industry will collapse by 2025 from about 10 per cent to about 5.5 per cent,” says Wagle, referencing data from McKinsey.

One of the reasons for this, he explains, is that after the financial crisis there were massive increases in the level of capital that banks have had to put aside, but the level of profit growth has not kept pace with the level of capital increases that needed to come about.

However, the threat the financial services industry face isn’t coming from fintech companies.

Like the pharmaceutical sector — where smaller biotechnology companies are providing the innovation for the pharmaceutical industry’s distribution channels — banks around the world have recognised that fintech companies can provide an engine for innovation and growth.

Banks are starting to collaborate with fintech companies so that the latest technology innovation can be channelled through the much larger distribution networks the banks can provide.

Instead, it is the platform companies — like the Chinese behemoths Alibaba and Tencent — that is placing the pressure on the industry.

Though these companies might have started life as a trading platform, they have moved into asset management and the provision of substantial financial services — satisfying multiple needs of the customer through a single platform.

When Ant Financial (the financial services subsidiary of Alibaba) lists, the expectation is that the “super unicorn” will be valued at US$150b — a similar size to Citigroup and twice the size of Wall Street titan Goldman Sachs.

The risk for financial services firms is that the more that can be done on a single platform, the greater the risk that people don’t step off that platform and do business through their bank. The risk banks now face isn’t just the possibility of marginal reductions in market share and the squeezing of margins, but rather the potential for “Kodak” moments — where huge chunks of a business completely disappear overnight.

Wagle is optimistic about the future, so long as banks begin implementing changes that will allow them to compete head on with the threat of disruption.

1. Implementing the new generation business architecture to provide extreme convenience

There is an architecture — which Wagle calls the “new generation business architecture” — that will enable banks to be more efficient, productive and informed than they currently are.

The four key technologies of this architecture are artificial intelligence (AI), cloud, blockchain and the Internet of Things (IoT).

“If banks do not introduce these technologies on an enterprise-wide basis, then they are going to be in some trouble,” says Wagle.

He says that aside from very mundane, routine tasks that are very low level, “we are a long way away from replacing people with AI”. However, one benefit that these technologies will provide is their ability to analyse research and data, augmenting and enhancing the capabilities of people.

“Where in the past you might have spent several days preparing for a meeting, you can now prep for that meeting within minutes,” says Wagle.

“In one of the engagements IBM did with relationship managers in wealth management, their productivity was enhanced eight times because they used technology to help with the research.”

The new generation business architecture will help banks to provide the level of convenience and immediacy that has become increasingly commonplace with technologies like Uber.

When someone makes an application for a loan, they do not want to be waiting days — let alone weeks — for the money to hit their account.

Wagle says that banks have done a very good job of creating customer apps, but the processes behind the apps and the technology that supports those processes is still often in the dark ages.

“There is still a lot of manual activity,” he says. “Banks should make use of technology and APIs [the software that essentially connects various entities’ systems together] to ensure the vast majority of banking processes can work together, so that they are able to provide an end-to-end digital experience.”

2. Offering services that go beyond banking

“If all you’re going to provide a customer is a loan then it is very fast going to become a commodity exercise, because they’re going to go from you to someone else to someone else and find the cheapest offer.

“We have gone past that era where you can schmooze an individual, form a relationship, and say that they are going to stay with you forever.”

Instead, banks should start thinking beyond banking, and create ecosystems.

As an example, Wagle explains that some banks are already able to provide a range of services when you ask for a mortgage.

Alongside the loan they can provide advice on where you should buy, what the community and schools are like, and what the valuation of the house should be.

They have an ecosystem around the house buying decision because they are helping the customer to buy a house — not only selling a mortgage.

“This provides a much stickier experience,” he says.

“Customers will make their decision on the quality of services they are receiving, instead of solely on what a bank is charging for the mortgage.”

3. Reducing costs with efficiency-boosting technology

When benchmarked against the global banking industry, the cost-to-income ratio for New Zealand banks is very low.

But, Wagle explains, that is not because New Zealand has a highly efficient banking industry, but rather because New Zealand’s margins are very high.

“Your margins are spectacular compared to other parts of the world,” he says.

He warns that if we get competition here it will start to compete the banking margin away.

“You are probably about 5-7 percentage points in cost-to-income ratio higher than where you need to be. What that then means is you’ve got to get somewhere between 22-25 per cent of your operational and IT costs out of the business — and the way to do that is through cloud.”

Cloud computing can cut as much as 40 per cent of information technology costs for banks, while also improving security and efficiency.

Though there is very little you can put in the public cloud in the financial services industry due to regulations and requirements on data privacy, banks can put their middle and back office workloads on to a hybrid cloud platform — something Westpac has done in Australia.

That is now driving 25 per cent out of their cost and has also given them real agility.

“Things that were taking 20-25 days to do before, they can now do in three or four days.

“It’s giving that speed that you need to have in order to really satisfy the customers in that kind of instantaneous way that has become so important,” he says.

Opportunity knocks

New Zealand banks have a massive benefit that the likes of Alibaba don’t — yet — have. Most of the data that is required to service the requirements of customers exists within the bank, and it will take new entrants a long time to get that information and to build trust.

There is only a limited window of opportunity. As open banking becomes a requirement around the world, banks will have to make their data available to any customer that wants the data to be provided to external providers and will lose their monopoly.

By addressing issues around customer services and convenience, thinking beyond banking, and operating at costs that are substantially lower (and therefore offering more competitive pricing), the financial services industry will be much more secure in the face of competition.

Leave a Reply

Want to join the discussion?Feel free to contribute!