The business climate has been anything but predictable over the past two years.

The Covid-19 pandemic has caused upheaval and seen companies scramble to adapt to a rapidly changing environment — the most visible changes have been the rapid uptake of digital technologies and the rise of remote and hybrid working.

That unpredictability looks set to continue, but there are several underlying trends for businesses to keep in mind as they navigate the year ahead.

A new era of geopolitics

In response to Russia’s invasion of Ukraine, the US and EU have cut selected banks from Swift and closed airspace to Russian planes. Further sanctions have been imposed on Russia’s central bank, aimed at preventing it from accessing reserves.

While the crisis might be on the other side of the world, the economic impact will ripple through the global economy and reach NZ shores.

Russia is the world’s second-largest exporter of crude oil and refined petrol, and the world’s largest exporter of natural gas. Global crude oil prices have already reached their highest levels since 2014, and it is expected that prices will go even higher as the conflict persists. This will impact fuel, supply chains, and the cost of goods in general.

Businesses should also brace for cyberattacks, which many predict Russia will use in response to sanctions. NZ’s National Cyber Security Centre (part of the GCSB) recently released an advisory encouraging nationally significant organisations to consider their security, exercise readiness, and monitor for relevant cyber security developments.

Closer to home, the South China Sea and China’s increasing influence in the Pacific continues to cause fractures in the relationship between China and the United States.

Just prior to the Beijing Winter Olympics in a joint statement, President Xi Jinping and Russian President Vladimir Putin denounced interference from the United States in their affairs and opposed further enlargement of Nato.

While New Zealand has so far managed to carefully navigate its relationship with China, we will face increased pressure as Australia, the United States and the UK make stronger statements about China’s behaviour. At last year’s Apec CEO Summit, President Xi warned Asia-Pacific nations to not “relapse into the confrontation and division of the Cold War-era”.

Prime Minister Jacinda Ardern noted at last year’s China Business Summit that differences between NZ and China were “becoming harder to reconcile” as Beijing’s role in the world grows and changes, and that “managing the relationship is not always going to be easy and there can be no guarantees”.

With geopolitics entering a new era, businesses must walk a geopolitical tightrope and be ready to respond as events occurring elsewhere in the world impact their own operations, relationships, and people.

Increased employee turnover becoming harder to prevent

Since the start of the pandemic, the “Great Resignation” has gained momentum. The pandemic has shifted the mindset of employees, and seen them leave their jobs in search for a better work-life balance, remote work opportunities, increased flexibility or higher pay. In some cases they are moving to organisations that provide a better sense of purpose and meaning, with values that align with their own.

In order to remain competitive and attract and retain workers, companies have to rethink the benefits they offer and clearly articulate their purpose.

This is particularly true for knowledge sectors — those industries significantly reliant on the use of technology and human capital. The tight labour market around the world has seen those workplaces that don’t offer the flexibility and purpose demanded by their employees hindered by increased turnover in a market where good talent is hard to find.

But remote and hybrid has introduced new challenges for business.

The removal of a commute dramatically increases the pool of potential companies for employees. Someone living in Taranaki can now apply for remote working roles in Wellington or Auckland that might have previously been unobtainable to them.

It also limits the social ties that employees make with colleagues.

We have all been to staff farewells where we are told by the departing employee “it is the people here that makes it so hard to leave this job”. These connections that might have once encouraged employees to remain in their job have become weaker and will see the great resignation becoming a sustained challenge for business to grapple with.

Four-day work week gaining momentum

As an alternative to negotiating remuneration with employees and becoming drawn into a bidding war with other workplaces, there has been a rise in companies offering a shorter work week as a bargaining chip.

One example of reduced hours is the four-day work week, which is gaining momentum around the world.

NZ’s Perpetual Guardian trialled a four-day week in 2018 — a world-first for a privately held company.

The eight-week experiment measured productivity, motivation and output, with staff paid the same amount for working fewer hours. It discovered productivity improved 20 per cent, and employees were more creative, committed and less stressed. It has since made the move permanent.

Perpetual Guardian founder Andrew Barnes says the four-day working week is “not just having a day off a week — it’s about delivering productivity, and meeting customer service standards, meeting personal and team business goals and objectives”.

More companies are now beginning to trial shorter work weeks.

A four-day week pilot in the United Kingdom begins in June, with 30 companies signed up so far. The pilot is run by 4 Day Week Global, an organisation that advocates for the shorter week. It says similar programmes are set to start in the US and Ireland, with more planned for Canada, Australia and New Zealand.

Wellness on the way up

Covid-19 has put significant strain on the workforce. Uncertainty around job security, lockdowns, social isolation and limited social contact all contributed to the mental health crisis and exacerbated stress, anxiety and depression for both employers and employees.

The challenge of retaining good employees has seen businesses and business leaders prioritise health and build a culture of wellbeing in the workplace that openly supports mental health.

Many organisations have introduced wellbeing programmes, which include partnerships with mental health providers, subscriptions to mental health apps, fitness classes and additional days off. Last year, Westpac New Zealand introduced five days a year of wellbeing leave, and NZX-listed Vista Group introduced half-day Fridays for all its staff.

Research conducted by the New Zealand Institute of Economic Research last year on behalf of Xero showed investing in employee wellbeing can help to make a business more profitable.

It estimated that for every dollar a small business invests in company-wide wellbeing initiatives for staff, it can expect to see a return of up to 12 times within a year.

The impact of Omicron (and future variants)

Overlaying all these trends, Covid-19 remains present. While the world welcomed the news that the highly transmissible Omicron variant is associated with less severe disease than earlier variants, a pattern of new variants around every six months has emerged.

Since there is a risk of the virus mutating each time it reproduces, the greater transmissibility from Omicron brings with it an even greater chance of new variants emerging.

It was hoped by many that the vaccine rollout would bring an end to the pandemic, but it looks increasingly likely that Covid-19 — in one form or another — is here to stay.

New tools like antivirals, antibody treatments and new vaccines are coming on board this year, which will help us navigate Covid-19 as it becomes an endemic disease.

These will be important as 2022 (hopefully) becomes the year that businesses, employers, employees and government finally reach post-pandemic normality. In a year fraught with challenges of all kinds to navigate, that is something that should bring hope to us all.

https://www.timmccready.nz/wp-content/uploads/2022/03/Business-trends-2022-Tim-McCready.jpg726501tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2022-03-03 11:06:072022-03-03 11:09:04Trends that matter in 2022 (NZ Herald)

When Kathmandu achieved B-Corp certification in 2019, it became the largest Australasian retailer to be certified through the stringent process which recognises the highest standards of environmental and social performance.

“Part of being a certified B-Corp is looking at how we can benefit everyone that our brand comes in contact with, from suppliers to customers,” says Kathmandu CEO Reuben Casey.

“It helps us on that path of continuous improvement and demonstrates to our customers, shareholders, investors and suppliers that we are committed to doing the right thing.”

The Deloitte Top 200 judges commended Kathmandu Holdings for putting sustainability right at the heart of its strategy, and say this is why Kathmandu has been recognised as the winner of the 2021 Sustainable Business Leadership award. They are impressed by the leadership it demonstrates across ESG (environmental, social, governance) to drive long-term value for its shareholders and for the planet.

The Kathmandu brand was established in 1987, with Kathmandu Holdings formed in 2009 as a publicly listed company. The subsequent acquisition of hiking footwear brand Oboz (2018) and surfwear brand Rip Curl (2019) has seen Kathmandu Holdings transform from an Australasian retailer to a brand-led global multi-channel business. The Group is now working to extend Kathmandu’s B-Corp accreditation across its other key brands — Rip Curl and Oboz.

“Sustainability is central to Kathmandu’s strategy and is felt by all divisions of the company,” says Top 200 judge and Direct Capital managing director Ross George. “We were impressed with this ‘whole of company’ involvement — it is transnational and embraced by the board, management, and all levels of staff.”

Last year, Kathmandu Holdings completed an ESG materiality assessment across the group, speaking with stakeholders about where it can do better and what it should be focused on.

It also recently secured NZ’s largest syndicated sustainability-linked loan. The A$100m loan is tied to ESG and will be measured against a reduction in greenhouse gas emissions, B Corp certification, and improving the transparency, wellbeing and labour conditions for workers in its supply chain. If targets are hit, the interest rate on the loan decreases.

The judges were impressed by the bold ESG targets Kathmandu has set out to achieve by 2025, as it continues to consider how it can improve at every touch point. One of these targets was to become carbon zero by 2025. Kathmandu reached this target four years ahead of schedule, after offsetting its operational carbon footprint through Toitū carbonzero certification.

Casey says while this is a huge step, Kathmandu will continue to work towards its larger goal of net zero environmental harm by 2025. In 2022, it will set science-based targets that align with the Paris Agreement, and will hold itself accountable to those targets.

“This forces us to really understand the wider impact across the wider supply chain and value chain, as opposed to just doing what we can control,” he says. “It also helps us to influence our suppliers a bit more as well.”

Another of Kathmandu’s targets is to have 100 per cent of its products designed, developed and manufactured using elements of circularity principles.

In a first step, last year Kathmandu released its Pelorus Biofleece, made from 100 per cent recycled fabric which can degrade by 93.8 per cent in landfills at the end of its life. Later this year, it will release a 100 per cent biodegradable down jacket, with every component of the jacket able to biodegrade in landfill and marine environments.

“We are trying to demonstrate leadership and push forward the boundaries of what is possible,” says Casey. Kathmandu Holdings’ other brands are making progress towards its aim to achieve B-Corp certification across the entire group.

Rip Curl undertook a carbon audit and established a new ESG team to reflect Rip Curl’s increased focus on sustainability and take steps toward B Corp certification. The business sources its sustainable cotton in line with the Better Cotton Initiative, and this year launched a wetsuit take-back programme.

Oboz has embarked on its first materiality assessment and carbon footprint audit. Over the next 12 months it aims to work aggressively to surpass the 80-point minimum requirement to become B Corp certified. The company plants a tree for every pair of footwear sold and has 95 per cent environmentally preferred leather materials in its product range.

Finalist: Lion

Country Director for Lion New Zealand Craig Baldie says the company’s success hinges on its ability to operate ethically and in the best interest of society, including looking after the environment.

The beverage brewer and manufacturer’s sustainability approach aims to strengthen the resilience of the communities in which it operates, champion responsible use of its products, and ensure its environmental legacy has a positive impact now and for future generations.

The Top 200 judges commended Lion for recognising the importance of operating ethically given the product they sell, and its focus on creating a balanced portfolio of products — including low and no alcohol options.

“Lion has been a New Zealand leader in creating a culture of responsible drinking which it calls mindful consumption,” says Top 200 judge Ross George. “It runs alcohol education programmes and is a member of the responsible drinking charity, Cheers.”

“On the employment front, Lion is an inclusive, flexible and diversified workplace.”

Baldie says Lion’s ability to operate is a privilege, not a right.

“Businesses who do the right thing for the long term are the ones that will endure,” he says. “For Lion as New Zealand’s largest alcohol beverage company, this means contributing to a positive and safe drinking culture is of primary importance.”

The judges were also impressed by Lion’s very direct commitment to the circular economy concept and its responsible practices in the supply chain, which are reflected in its commitment to a net zero value chain by 2050. This involves partnering with suppliers to measure and reduce collective lifecycle emissions.

As part of this strategy, Lion has committed to use 100 per cent renewable electricity to brew its beers by 2025 and has further stretched itself by adapting its existing science-based target to limit global warming to under 1.5 degrees. This sets a reduction target of 55 per cent by 2030 for its direct emissions from a 2019 baseline. The circular economy concept is embedded in Lion’s business performance and targets, as well as parent company Kirin Holdings’ Environmental Vision 2050.

The judges note that Lion has already made good progress.

Since 2015, it has achieved a 28 per cent absolute reduction in its carbon footprint. It has become the first large-scale carbon neutral brewer in both Australia and New Zealand and New Zealand’s largest beverage manufacturer to be certified as carbon zero.

One of its core brands, Steinlager, became New Zealand’s first large-scale beer brand to achieve carbon zero certification. To reach this milestone, Lion says it focused on reducing emissions throughout Steinlager’s product lifecycle — from growing the hops and barley, and brewing the beer, to packaging and transport.

Lion has also invested in water efficiency initiatives, reduced its waste, and is making its packaging more recyclable and reusable. Already over 97 per cent of Lion’s packaging materials are recyclable and it is targeting 100 per cent of packaging to be reusable, recyclable, or compostable by 2025.

Finalist: Synlait Milk

Synlait Milk has bold ambitions to be “net positive for the planet” and instrumental in its industry’s response to climate change — a significant feat given agriculture is responsible for 30 per cent of the world’s greenhouse gas emissions and 70 per cent of freshwater use.

Synlait combines expert farming with state-of-the-art processing to produce a range of nutritional milk products for its global customers. It has put sustainability at the centre of its corporate purpose, and in 2018 set 10-year targets and an aspiration to become B-Corp certified — which it achieved last year.

“When we set these bold goals for ourselves, we didn’t know how we would achieve them,” says Hamish Reid, Synlait Director for Sustainability, Brand, Beverages and Cream.

“We are on track to beat our targets that no one thought we would achieve, and beat the timeframe as well. It’s an example of when you are really brave and put yourself out there, people galvanise around that.”

The Top 200 judges say Synlait’s executives are backing ESG strongly, and as a result the company scores well on these metrics.

“In a challenging year for the company, its focus on sustainability has not waned and it remains an industry leader with ambitious ESG targets,” says Top 200 judge Ross George.

“These are ambitious targets, both on-farm and off-farm, and have recently been updated under the Science Based Targets initiative.”

One of these targets is a reduction in emissions from the manufacturing process. Synlait is transitioning to renewable energy and has committed to not build another coal-fired manufacturing facility. A trial last year to replace a coal boiler with renewable biomass has progressed to become a permanent project.

“We now have a very clear path forward. From next financial year, we are commencing our rapid transition off coal,” says Reid. “Our original intention was early next decade, but we now think this will be entirely feasible as early as 2024 or 2025.”

Synlait works with its farmer suppliers to evolve New Zealand’s reputation as a responsible and sustainable producer of food, and help farmers understand how their management of the farm impacts on greenhouse gas emissions.

“This allows us to attract the most innovative farmers that are thinking about the future of the food system and where transitions might be happening,” says Reid. “It immediately gave us a greater supply base, because people were really interested in understanding and working together with the processor on how they might future-proof their businesses for success.”

This has resulted in on-farm emissions intensity, per kg of milk solids, reducing 5 per cent over the last year, or 10 per cent compared to its 2018 base year when its targets were first established.

Total off-farm emissions have remained stable since last year, however the emissions intensity, per kg of product, has reduced by 24 per cent compared to 2018.

“No one thought we would achieve what we have — including ourselves,” says Reid. “We didn’t think it would be possible to reduce our emissions by 10 per cent, and we have already hit the Government’s 2030 target.”

https://www.timmccready.nz/wp-content/uploads/2022/03/Sustainable-Business-Leadership-2021-Kathmandu.jpg729496tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2022-03-03 11:02:092022-03-03 11:09:38Dynamic Business: Sustainability central to strategy (NZ Herald)

Patrick Strange’s positive and inclusive style, together with his proactive leadership role in the business community, saw him crowned as this year’s Chairperson of the Year at the Deloitte Top 200 awards.

During 2021, Strange led a group of senior business leaders that called on Government to be more transparent about its plans to get New Zealand to a “Covid normal”. He says he was motivated to speak up because he was concerned Government was failing to build a long-term strategy.

“We were complimentary about the Government on things they had done, but we did criticise them,” he says. “That is the role of business, that is the role of all New Zealanders — open debate.”

The Deloitte Top 200 judges say Strange is very effective in building relationships with Government for the organisations he chairs — Chorus and Auckland International Airport — which is vital given their importance in New Zealand’s infrastructure landscape.

Chorus has played a critical role over the past year with its fibre network, which has been under significant load with so many New Zealanders working from home during the lockdown.

“We were still connecting 800-900 customers a day, with Covid and all its restrictions,” Strange says. “We don’t hear about it, but they have done a great job not missing a beat under those constraints and added layers of difficulty.”

Strange pushed back on the Commerce Commission over its proposed price control settings for the provider’s ultrafast broadband network, and the returns it should be allowed to make on its regulated asset base. In a letter to the commission, he warned of “regulatory failure” if Chorus was prevented from earning a fair return on its investment.

“We are there to represent New Zealanders — and particularly our shareholders — and I call that out,” says Strange. “I have a constructive relationship with the Commerce Commission and get on well with them — but they know if I disagree with them, I will say it publicly.”

Judge Cathy Quinn, an independent director herself, says this has no doubt been agonising to deal with and required Strange to be heavily involved. But it is clear he did a good job that will allow Chorus to continue to invest in innovation and deliver a fair return to shareholders.

For Auckland International Airport, Strange says the biggest challenge in 2020 was its huge loss of income and the need to rapidly raise capital to redress the balance sheet. But the past year has been much more about people — particularly those that have had to continue operating remotely, which has put a lot of strain on them.

“We are spending a lot of time worrying about how to support people,” he says. “The uncertainty — the way they are having to work — they are working long hours in difficult circumstances.”

His biggest challenge for both companies he chairs has been the loss of exchange that comes from meeting face-to-face. This was also noted as a big challenge by other finalists in this category.

“We can operate well on Zoom, but nothing beats getting together and the things you learn by walking around and talking to staff,” he says.

The judges highlight this emphasis on people as another of Strange’s core strengths. “Patrick is highly regarded by his peers, the management teams he works with and broader stakeholders as an inclusive chair who brings out the best in his fellow directors and management teams,” says Quinn.

“He encourages others to contribute and offers his perspective in a constructive way.”

Strange says this isn’t hard to achieve, because he enjoys working with talented and motivated people — from fellow directors to the impressive young people involved in the companies he chairs.

“We are there to have fun, and I am just part of that,” he says. “I am just lucky enough to oversee a couple of great companies where we have that culture.”

Finalist: Barbara Chapman

Barbara Chapman’s governance career has been shaped by her interest in transformation and improving the experience of customers.

She is chair of Genesis Energy and NZME, and is a director of Fletcher Building and BNZ. Chapman is also deputy chair of public-policy think tank The New Zealand Initiative and was chair of the Apec 2021 CEO Summit. In 2019 she was awarded a Companion of the New Zealand Order of Merit (CNZM) for services to business.

When Chapman joined the NZME board in 2018, it had an enormous amount of debt. “That was really shackling the company from being able to do what it needed to do to grow,” she says.

NZME is now debt-free, succeeding in a three-year plan to eradicate $100m in debt. Its share price reached a high of $1.46 on December 15, up dramatically from its depths of $0.18 at the start of the pandemic.

“Along the way, we were balancing dropping debt with investing in things like premium, and the technology you need to drive that,” says Chapman — recognising that having cash now gives NZME far more scope to invest, such as its recent acquisition of BusinessDesk.

Judge Cathy Quinn says Chapman has shown remarkable skill while working with the board and management team of NZME throughout its transformation.

“Since joining the NZME board in 2018, Barbara has played a key role in the company’s turnaround after financial challenges and helped set foundations for future success.”

The judges also acknowledge Chapman’s leadership in astutely navigating Genesis Energy through the August power outages, as power distributors responded to Transpower’s demand to reduce the burden on the national grid. A ministerial inquiry has since shown that Genesis was wrongly blamed at the time. “As it came out, we didn’t cause any of the problem and we couldn’t have done anything different,” says Chapman. “But given we are 51 per cent owned by the government, quite rightly they were asking us some pretty strong questions.

As for her highlight over the past year, Chapman points to the success of the Apec CEO Summit, held at the end of 2021.

Soon after taking on the role at the request of the Prime Minister, a fire broke out at the International Convention Centre — the intended venue for the summit. Then Covid-19 struck, thwarting plans to host thousands of delegates in-person.

“To deliver an online event that had the reach it did, as well as the response it had, has been amazing,” she says. “I am really proud that we focused hard on gender balance and diversity with our speakers, and people tell us we ended up with what was the best CEO Summit ever. Over 3000 people watched it — amazing for something online!”

Finalist: Mark Tume

Mark Tume says boards are decision-making engines, and that there is a ‘secret sauce’ in the boards he chairs that makes the whole greater than the sum of its parts.

“To get the most out of a board, it is not about me being a leader, it is about arranging a meeting so you can get the most out of everyone and a contribution from everyone.”

Tume is chair of infrastructure investor Infratil and commercial arm of Taranaki’s largest iwi, Te Atiawa Holdings. He is also a director of Retire Australia, Precinct Properties and was chair of Ngāi Tahu Holdings Corporation until December 2021.

The Top 200 judges say Tume’s performance at Infratil has been excellent, as has been his significant contribution to the Māori economy.

“Tume was pivotal in establishing Te Atiawa Holdings, a new entity being built from the ground up,” says Quinn. “He has been on the Ngāi Tahu Holdings board in three separate instances, stepping down as chair at the end of last year.”

Tume says Māori organisations have a clear view that assets, investments and returns should be seen as multigenerational. He says there’s a real alignment between that thinking and Infratil, due to the nature of the assets needing to last a hundred years or more.

In December 2020, AustralianSuper, Australia’s largest pension fund, put in a takeover bid for Infratil worth nearly $5.4 billion — representing a 22 per cent premium on its closing share price at the time. The takeover bid resulted in a 20 per cent jump in Infratil’s share price, and was ultimately rejected. Tume says the offer materially undervalued Infratil’s high-quality and unique portfolio of assets.

“It wasn’t a hard decision, AustralianSuper’s offer wasn’t a huge premium,” he says, noting Infratil has returned an average annualised shareholder return after tax and fees in excess of 18 per cent since its inception.

“Tume’s ability to navigate challenging issues such as a hostile takeover bid from Australia and remain steadfast in his belief that the offer materially undervalued Infratil’s portfolio, is a clear demonstration of his focus to do what is best for shareholders,” says Quinn.

Infratil also dealt with another significant transaction in the past year — the sale of wind farm operator Tilt Renewables. “We had a tremendous number of board meetings, because we were dealing with a $5b takeover offer at the same time as a $3b sale process of Tilt Renewables,” Tume says. Ongoing restrictions of Covid and the border closure added to the pressure since both deals were run out of Australia.

While this period was a huge challenge due to the need to deal with so many things at the same time, including a change in CEO, completing the Tilt deal was also one of Tume’s highlights of the past year.

“You don’t get many years like this one where so much pressure and stress and bad things are happening — and yet everything lines up so nicely.”

https://www.timmccready.nz/wp-content/uploads/2022/03/Chairperson-of-the-year-2021.jpg732503tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2022-03-03 10:57:092022-03-03 11:09:51Dynamic Business: Chairperson of the Year – Patrick Strange (NZ Herald)

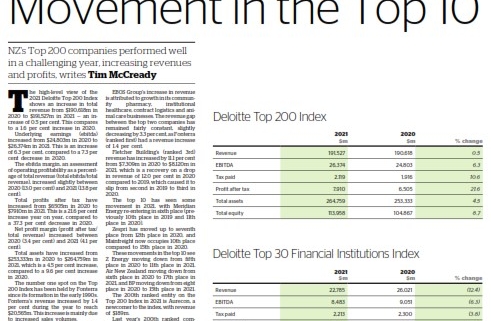

The high-level view of the 2021 Deloitte Top 200 Index shows an increase in total revenue from $190,618m in 2020 to $191,527m in 2021 — an increase of 0.5 per cent. This compares to a 1.6 per cent increase in 2020.

Underlying earnings (ebitda) increased from $24,803m in 2020 to $26,374m in 2021. This is an increase of 6.3 per cent, compared to a 7.3 per cent decrease in 2020.

The ebitda margin, an assessment of operating profitability as a percentage of total revenue (total ebitda/total revenue), increased slightly between 2020 (13.0 per cent) and 2021 (13.8 per cent).

Total profits after tax have increased from $6505m in 2020 to $7910m in 2021. This is a 21.6 per cent increase year on year, compared to a 37.3 per cent decrease in 2020.

Net profit margin (profit after tax/total revenue) increased between 2020 (3.4 per cent) and 2021 (4.1 per cent).

Total assets have increased from $253,333m in 2020 to $264,759m in 2021, which is a 4.5 per cent increase, compared to a 9.6 per cent increase in 2020.

The number one spot on the Top 200 Index has been held by Fonterra since its formation in the early 1990s. Fonterra’s revenue increased by 1.4 per cent during the year to reach $20,565m. This increase is mainly due to increased sales volumes.

EBOS Group has maintained its number two ranking, increasing its revenue by 7.0 per cent from $9,241m in 2020 to $9,886m in 2021.

EBOS Group’s increase in revenue is attributed to growth in its community pharmacy, institutional healthcare, contract logistics and animal care businesses. The revenue gap between the top two companies has remained fairly constant, slightly decreasing by 3.3 per cent, as Fonterra (ranked first) had a revenue increase of 1.4 per cent.

Fletcher Building’s (ranked 3rd) revenue has increased by 11.1 per cent from $7,309m in 2020 to $8,120m in 2021, which is a recovery on a drop in revenue of 12.0 per cent in 2020 compared to 2019, which caused it to slip from second in 2019 to third in 2020.

The top 10 has seen some movement in 2021, with Meridian Energy re-entering in sixth place (previously 10th place in 2019 and 11th place in 2020).

Zespri has moved up to seventh place from 12th place in 2020, and Mainfreight now occupies 10th place compared to 15th place in 2020.

These movements in the top 10 see Z Energy moving down from fifth place in 2020 to 11th place in 2021, Air New Zealand moving down from sixth place in 2020 to 17th place in 2021, and BP moving down from eight place in 2020 to 15th place in 2021.

The 200th ranked entity on the Top 200 Index in 2021 is Aurecon, a newcomer to the index, with revenue of $189m.

Last year’s 200th ranked company, Airwork, had revenue of $200m. This is a 5.4 per cent decrease in revenue between 200th ranked companies year on year.

Top profits

Fonterra (ranked first in the Top 200 Index) reported the top profit for 2021 at $532m. Last year’s top profit was also held by Fonterra, reporting a net profit of $803m in 2020. This top profit amount has decreased by 33.7 per cent year-on-year.

The decrease in Fonterra’s 2021 profit is attributed to non-recurring gain on sale of investments which boosted the 2020 profit by $467m. This has been offset by lower net interest-bearing debt and an increase in sales revenue for Fonterra in the current year.

In contrast, average profit after tax across all 200 companies has increased from $32.5m in FY20 to $39.5m in FY21, a 21.5 per cent increase.

Respiratory products maker F&P Healthcare (22nd) has moved up to second place in 2021, from sixth in 2020, with profit after tax increasing by 82.6 per cent from $287m in 2020 to $524m in 2021.

Auckland Airport (139th) has moved up to third place in 2021, from 14th in 2020, with profit after tax increasing by 139.2 per cent from $194m in 2020 to $464m in 2021.

Meridian Energy (6th) has moved up to fourth place in 2021, from 15th in 2020, with profit after tax increasing by 143.2 per cent from $176m in 2020 to $428m in 2021.

Ryman Healthcare (97th) has moved up to fifth place in 2021, from 7th in 2020, with profit after tax increasing by 59.6 per cent from $265m in 2020 to $423m in 2021.

Infrastructure investor Infratil (38th) has moved out of the top profits, from being placed second in 2020, reporting a profit after tax of $509m in 2020, to reporting a loss of $88m in 2021.

Biggest losses

The biggest loss for 2021 was reported by hydrocarbon producer OMV (ranked 83rd in the Top 200 Index), with a loss of $567m.

OMV’s loss is a $614m drop from its 2020 profit after tax of $47m.

Pacific Aluminium (58th) and Air New Zealand (17th) respectively hold the second and third biggest losses in 2021.

This is reasonably consistent with the loss positions they occupied last year.

Pacific Aluminium was third and Air New Zealand was first in the biggest losses for 2020.

Air New Zealand’s continued losses are reflective of the decline in profits of the air travel industry caused by the impact the Covid-19 pandemic has had on border restrictions limiting international travel.

Tasman Steel (54th) and Lion (71st) respectively hold the fourth and fifth biggest losses in 2021.

Kiwirail (64th) has moved out of the top biggest losses, from being placed second in 2020, reporting a loss of $325m, to having a profit in 2021 of $43m.

Most improved profit

Agricultural co-operative company Ravensdown (ranked 63rd in the Top 200 Index) recorded the most improved profit out of all the entities on the Top 200 Index.

It delivered a 10,213.8 per cent increase in profit from a $0.2m loss in 2020 to a $15.4m profit in 2021. Haier (30th) has the second most improved profit, recording a profit of $29.3m in 2021 compared to a $0.6m profit in 2020.

This is an increase of 4,834.3 per cent.

NZPM Group (144th) holds third place for most improved profit, with an increase of 2,404.8 per cent. In the current year, NZPM Group recorded a profit of $6.8m, compared to a 2020 profit of $0.3m.

There is no overlap in the most improved profit list in 2021 relative to 2020.

Most improved revenue

Meat company Hellers (ranked 141st in the Top 200 Index) has reported the most improved revenue, increasing revenue to $269m in 2021 compared to $101m in 2020.

This increase has seen Hellers enter the Top 200 Index for the first time.

Newcomer to the Index, Wilmar Gavilon (143rd), is ranked second for most improved revenue. Wilmar Gavilon had reported revenue of $172m in 2020 which has now increased to $267m in 2021, representing a 55.1 per cent increase in revenue.

Fisher & Paykel Healthcare (22nd) has seen a similar increase in revenue, reporting an increase of 53.0 per cent from $1,273m in 2020 to $1,948m in 2021 which places it third for most improved revenue. Fisher & Paykel Healthcare occupied 16th position for most improved revenue in 2020.

Microsoft (72nd) is the only other company to be included in the most improved revenue index for two years in a row.

A2 Milk and Xero had been included in the most improved revenue index for the last four years, however they are not included in 2021.

Pushpay (142nd), My Food Bag (196th), Synnex (190th) and Tasman Liquor (152nd) are new entrants to the Deloitte Top 200 Index in 2021, and also feature in the most improved revenue index.

Hellers, Microsoft, Precinct Properties, Synnex and Tasman Liquor are included in both the most improved profit and most improved revenue index in 2021.

Top return on assets

Return on assets (ROA) provides an indication of how efficiently a company manages its assets in order to generate earnings. It is calculated by measuring profit against total assets reported.

Lotto NZ (ranked 26th in the Top 200 Index) holds the top spot for ROA for the third year in a row after newly entering the Top 200 Index in 2019. It has maintained a strong ROA of 194.7 per cent in 2021 compared to 214.0 per cent in 2020. The high ROA is driven by a 25.5 per cent increase in profit after tax from $333m in 2020 to $378m in 2021, with total assets of $199m in 2021.

Holding the second spot for ROA for the second year in a row is TAB (121st) – despite a decrease in its ROA to 94.5 per cent from 102.6 per cent. This is driven by an increase in total assets from $136m in 2020 to $208m in 2021, and an increase in profit after tax from $137m in 2020 to $163m in 2021.

Third place is held by newcomer Aurecon (200th) with a ROA of 35.3 per cent.

Fisher & Paykel Healthcare (22nd) placed fourth in terms of ROA, rising from fifth place in 2020. Its ROA has increased from 21.8 per cent in 2020 to 29.9 per cent in 2021, which is consistent with its increase in profit.

The general trend of increasing return on assets falls in line with the 21.6 per cent increase in average profits, with third to 20th places for 2021 increasing year-on-year against third to 20th places in 2020. Only Lotto NZ and TAB, ranked first and second respectively, saw a reduction in ROA year-on-year.

Top return on equity

Return on equity measures how effectively a company can generate income relative to the amount of money shareholders have invested in the firm.

It is a useful tool for investors, particularly when comparing firms within the same industry and is calculated by measuring the revenue earned against the average equity held over the past two years – to prevent changes in shareholder contributions skewing the results.

Lotto NZ (ranked 26th in the Top 200 Index) has taken the top spot for return on equity, moving from second place in 2020, with a return on equity percentage of 661.8 per cent.

TAB (121st), has moved up from third place to second place for its return on equity of 416.5 per cent.

Bunnings (31st) has dropped from top spot to third place with a return on equity of 264.7 per cent for 2021.

Kiwifruit marketer Zespri (7th) has risen to fourth place from sixth, with a return on equity of 105.0 per cent.

Nestle (90th) has maintained its fifth-place spot with a return on equity of 101.9 per cent.

The newcomers

This year, 22 companies were added to the Deloitte Top 200 Index. This compares to last year when 13 companies debuted on the Index.

Heinz entered the Index at the highest rank (ranked 56th in the Top 200 Index) with revenue of $768m.

Also entering the Top 200 Index within the top 100 companies were metals distributor and processor Vulcan Steel (59th) with revenue of $732m, and New Zealand Health Group (70th) with revenue of $639m.

Just missed the cut

The 200th place in the 2020 Deloitte Top 200 is Aurecon, which recorded $189m in revenue. In last year’s Top 200 Index, Airwork was ranked 200th with revenue of $200m in 2020.

Abano Healthcare (ranked 201st in the Top 200 Index), Whakatane Mill (202nd) and Wilson Parking (203rd) just missed the cut by $1m. Scott Technology (204th), Suzuki (205th) and China Merchant Properties (206th) were close to breaching into the Top 200 Index in the current year, all achieving revenue around the $186m mark. Of these companies, Abano Healthcare and Scott Technology have fallen out of the Top 200 in 2021, previously holding 168th and 182nd place in 2020 respectively.

In last year, not now

After its entrance in the Top 200 Index in 2019, Scentre wasn’t in this year’s index (in 2020 it ranked 90th). Until last year, the owner and operator of Westfield retail destinations was in the most improved performance index for two years in a row.

Shell has also dropped out of the index this year after ranking 149th in 2020. In 2019 it appeared in the top profit index, recording a figure of $1,397m.

Kordia didn’t feature in the Top 200 index this year. In 2020 it reappeared on the index ranked 183rd, after falling from the index again in 2019.

Horizon Energy (2020: 163rd) and Scott Technology (2020: 182nd) also did not make the list this year after entering last year’s index.

https://www.timmccready.nz/wp-content/uploads/2022/03/Deloitte-Top-200-2021-Tim-McCready.jpg407491tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2022-03-03 10:56:042022-03-03 11:10:15Deloitte Top 200: Movement in the Top10 (NZ Herald)

Infratil has been crowned Company of the Year and Skellerup’s David Mair named Chief Executive of the Year at the prestigious Deloitte Top 200 Awards.

Rocket Lab founder, CEO and chief engineer Peter Beck took out the coveted Visionary Leader award.

In its 32nd year, the Deloitte Top 200 Awards are a showcase of the very best of New Zealand business and business leaders. They celebrate the depth and range of our business community, featuring the industries and sectors that underpin our country’s success.

This year, the awards recognise outstanding results despite the ongoing challenges resulting from Covid-19, including companies and leaders from the manufacturing, retail, media, and energy sectors, all showcasing their commercial strength and agility during challenging times.

Infratil had an outstanding year in 2021, further enhancing its reputation as a savvy infrastructure and utilities investor. The company was active with its portfolio, divesting Tilt Renewables and investing in diagnostic imaging firm Pacific Radiology.

The panel of high-profile judges — convened by NZME editorial director of business Fran O’Sullivan — said Infratil’s combination of strong performances with its investment companies, especially data centres, along with its divestments and new acquisitions have added significant shareholder value over 2021.

“In addition, the company went through a fairly seamless transition of CEO from Marko Bogoievski to Jason Boyes and won the takeover battle with Aussie Super,” say the judges.

“While Infratil has been an excellent long-term performer, its total shareholder return of 65 per cent stands out.”

Another long-term performer is Skellerup Holdings, and this year its CEO David Mair took out the award for Chief Executive Officer of the Year.

The designer, manufacturer and distributor of engineered products has been led by Mair for over 10 years, and during his tenure has achieved significant revenue and earnings growth by focusing on designing and delivering critical engineered products for OEM customers.

“David is a steady pair of hands at Skellerup,” say the judges.

“He has a knack for presenting a soft, inclusive, popular leadership style with people and in strategy, but has a hands-on near fanatical knowledge of process, plant and equipment, and design for Skellerup’s manufacturing customers.”

The Visionary Leader award is one of just two awards made without finalists. This year, the award went to founder, CEO and chief engineer of Rocket Lab, Peter Beck.

The judges recognised Beck for taking New Zealand into the world of space and becoming a global leader who is redefining the space industry with ambitions that now stretch as far as Mars and Venus. Last August, Rocket Lab listed on the Nasdaq, where its market capitalisation climbed to $7.33 billion as it raised $1.14b to fund the next phase of Beck’s bold space journey — a proud Kiwi moment and bold visionary leadership from a ‘boy from Invercargill’.

Having been a finalist in the category in 2020, Patrick Strange was named this year’s Chairperson of the Year. Chair of Auckland International Airport and Chorus, he is highly regarded as an inclusive chair who brings out the best in his fellow directors and management teams.

The judges say that over the past year, Strange has taken a leadership position in the New Zealand business community by speaking up on areas where it might not have been easy — including on aspects of the Government’s Covid-19 response. He also responded robustly to aspects of the Commerce Commission’s proposed price and quality control settings for Chorus’ ultrafast broadband network.

Mercury’s William Meek has been awarded Chief Financial Officer of the Year. Meek’s career with Mercury spans 20 years and he has served as CFO for almost 15 of those, coming into the role prior to the successful float of the company in 2013.

The judges describe Meek as a highly competent CFO who thoroughly understands the financial statements of Mercury and knows how it creates value.

“Meek has delivered exceptional long and short-term impacts for Mercury,” they say. “He supported the company’s CEO in delivering superior shareholder returns and in 2021 helped execute Mercury’s successful efforts to enhance its presence in renewable generation and retail sales through two strategic acquisitions.”

NZME took out the Most Improved Performance award this year. The integrated media company – owner of the NZ Herald, Newstalk ZB, property website OneRoof and a suite of entertainment radio brands – has put a plan in place to transform into a digitally focused media business, and this turnaround strategy has seen digital revenue play an increasingly significant role in the company’s earnings.

“The market has responded positively to this strategy, with the share price climbing from a low of 18 cents in April 2020 to above $1.40 by the end of 2021,” say the judges.

Vulcan Steel has been recognised with the Best Growth Strategy award. The judges say the steel distribution company’s growth strategy has resulted in superior absolute and relative performance in the highly competitive steel distribution sector on both sides of the Tasman.

“It has executed both parts of its growth programme well with an annual revenue growth of 8 per cent and net profit growth of 38 per cent posted in the last five years,” they say.

“Vulcan is on track for another record year in 2022.”

Tourism Holdings’ Ollie Farnsworth has been awarded the title of Young Executive of the Year. With the tourism industry facing significant challenges in the last 18 months, Farnsworth approached tough issues of cost reduction and revenue generation with a constructive outlook in his role as chief commercial & customer officer.

“An innovative mindset has seen Ollie identify and effectively execute on new business opportunities including the well-known Get Moving to Get New Zealand Moving campaign,” say the judges. “His energy and empathy for customers and his people shines through in his leadership approach.”

Te Rūnanga o Ngāi Tahu (Ngāi Tahu) took out the Diversity and Inclusion Leadership award for its Cultural Confidence Programme, an innovative and comprehensive response to a very specific diversity and inclusion challenge.

“Mō tātou, ā, mō kā uri a muri ake nei — For us and our children after us’ — had the unintended consequence of raising doubts in the minds of their staff who are not of Ngāi Tahu descent, about the company’s commitment to them,” said the judges.

Kathmandu won the Sustainable Business Leadership award, which recognises businesses working toward the creation of long-term environmental, social and economic value.

The judges also chose to award a special judges’ award to Air New Zealand, in recognition of the airline’s efforts of the past two years. The judges praised all the airline’s employees who have strived to respond to the enormous challenges brought about by Covid-19, and in doing so have maintained strong support for the brand and service offering of the airline.

https://www.timmccready.nz/wp-content/uploads/2022/03/Deloitte-Top-200-2021-winners.jpg781726tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2022-03-03 10:54:382022-03-03 11:04:21Deloitte Top 200 awards: Top business leaders crowned (NZ Herald)

Before the end of this year, the Government will decide on the route, mode, and delivery for the project for the light rail project, which will run between Auckland’s city centre and Māngere, connecting majoremployment hubs in the city and the airport at each end.

Transport Minister Michael Wood acknowledges the decision has been a long time coming. He first launched the promise of light rail during his campaign for the Mount Roskill by-election in 2016 which brought him into Parliament. Labour campaigned on light rail at the 2017 election, but the move was stymied by Labour’s coalition partner New Zealand First in the last term of Government.

“It is no secret that it was in a fairly challenging stage at the end of the last term, and it had the political knockback between parties,” Wood says. “We had to have a reset which is effectively what happened this year. But it’s put us in a good position to take it to the next stage.”

The three options under consideration are:

• Light rail, a modern tram on city streets;

• Light metro, underground in a tunnel under the isthmus, and underground in Māngere and Onehunga, and at street level in other areas; and

• Tunnelled light rail, underground from Wynyard Quarter to Mt Roskill, and then up at street level to Auckland airport.

They were chosen after an assessment by the Auckland Light Rail team from over 50 different options for modes and routes against the project’s three objectives: improving accessibility, reducing Auckland’s carbon footprint, and unlocking urban development in the corridor.

Not a simple decision

The Auckland Light Rail project team say tunnelled light rail from Wynyard Quarter to Mt Roskill is their recommended option, as it gives the best transport and urban benefit, with the least disruption and the best fit with the network in future. Wood says this first line will provide a base for the additional Waitematā harbour crossing and a line to the Northwest.

“It’s also important to understand that this is just the start of light rail lines in Auckland to create a joined-up rapid transit network with our separated bus lanes and heavy rail network — all of which we are currently extending and upgrading.”

The three options will be able to accommodate between 19 and 24 per cent of Auckland’s growth along the corridor. The key thing about that is it supports us with housing growth, but it also supports us with a more compact urban form,” says Wood.

“This is actually one of the more structural things that we can do to reduce emissions, because if you put someone on the fringes of the city, by definition, many of their journeys are going to be long journeys.

“If you build houses next to an amazing rapid transit network, close to schools, employment and recreation, people are going to emit much less by definition.”

Each of the three options enable a mode shift away from private vehicles and therefore a reduction in Auckland’s carbon emissions.

The light metro and tunnelled light rail options encourage higher numbers of people and therefore result in fewer emissions, however light rail on the surface has less embedded carbon because less concrete and steel is involved in the construction.

“We get to a point of carbon neutrality and start reducing carbon more quickly with surface light rail, but over the long run the others catch up,” says Wood. “At 2050, surface light rail is the better option for carbon reduction, but over the long-run, the others are.”

Cabinet’s decision later this month will weigh up all aspects including climate, cost, disruption, value for money, and the ability to open up housing. “I want to be clear with the trade-offs,” says Wood, “and in this case, it’s not a simple one.”

Opportunity for the private sector. But no PPP

Wood says a public-private partnership (PPP) has been ruled out for the Auckland light rail project, with Cabinet having already decided it will be taken forward using a public service delivery model. This is partly due to the previous iteration of the project floundering during the PPP selection process. Wood says many months could have been spent debating the merits of the delivery model, but for him, the most important thing is to move forward and deliver it.

He adds he also has a personal view that bringing PPP into public transport projects is a little more complex, “because the integration with existing networks and existing public transport operations is more complex if you have another player in the mix.”

Wood says the Government is open to PPPs when it stacks up, but stresses that there are “significant opportunities for investment right across the board” for the private sector for this project and other transport projects across New Zealand.

This will be the biggest transport project in New Zealand’s modern history, and the start of a broader programme of investing in mass rapid transport, beginning a pipeline of city-wide mass rapid transit work over the coming 20-plus years. That’s the first time we’ve really been able to say that as a Government,” he says.

“It offers industry the opportunity to start doing some forward planning. Obviously, the core transport infrastructure job needs to be done that will require both a high level of technical expertise, but also just a lot of work, as well.

“From the broader planning and urban design community, there will be a wholesale urban regeneration along this corridor that will offer opportunities for investment in commercial property, residential property — we are talking about an urban uplift of between 20,000 and 35,000 houses along the corridor.”

Community engagement encouraged

Wood says engagement from the community will be important for the project to succeed, and is a core part of the Light Rail team’s remit.

It has already been gathering the views of Aucklanders, and has found considerable excitement about light rail and the reduction in carbon footprint. But there are concerns about affordability of use, construction disruption and environmental, cultural, civic and heritage impacts.

He says the master planning phase of the project will be a critical point at which communities are brought in to share their views on what the vision should be for various communities and town centres along the light rail route.

“We want to hear the vision for communities in Eden Terrace, Mt Roskill and Onehunga over the next 50 years, and how we can bring together transport with housing, public open spaces and lively town centres.”

Auckland’s 2050 public transport network

Transport Minister Michael Wood says his vision for Auckland’s transport network in 2050 is one that is clean, carbon-neutral, and connects and enhances communities — instead of bypassing and gutting them, “as our transport network sometimes has in the past. It supports a high level of good quality, compact urban growth, and enables more affordable, accessible places for people to live.

“Fundamentally it enables a good standard of living and enables connection to employment, recreation and to other things that are important for people’s lives.”

But the key, Wood says, is for a genuinely linked-up public transport network across all aspects of the region that people and freight can move around efficiently.

“That’s something we haven’t ever quite cracked in Auckland.

“But it’s something that all grown up, successful international cities have.”

Three options for light rail

Light rail: consisting of modern trams running on tracks embedded into the road but separated from traffic. It would travel totally on the surface. Sometimes that would be on roads and sometimes along the motorway.

The Auckland Light Rail team investigated Light Rail on Dominion Road and on Sandringham Road, and on balance, its investigations favoured Dominion Road.

One consideration was that a light rail route on Sandringham Road would require a significant power cable to be relocated to Dominion Road, which would delay works by up to two years and would mean that businesses and residents on both Dominion Road and Sandringham Road would be affected by construction disruption.

Light metro: a rail-based mode that is grade-separated (it is elevated or underground).

The Light Metro option would travel through tunnels built under densely populated urban areas and on the surface through non-urban areas, such as motorways.

Tunnelled light rail: like light rail, this option would also consist of modern trams, but would be partly tunnelled from Wynyard Quarter to Mt Roskill, with the balance of the route running on the surface (on roads and sometimes along the motorway). It would incorporate underground stations in the city centre and on the isthmus including the University precinct.

For the tunnelled portion, the alignment does not need to follow the road, so the actual route and station locations would be developed in the detailed planning phase, including through consultation with communities, iwi and stakeholders.

History of light rail in Auckland

1902-1956

Electric trams ran from downtown at the Waitematā Harbour and across to Onehunga on the Manukau Harbour. They were then the world’s only coast to coast tramway system.

1956

The decision was made to rip up the tramlines and use buses.

Late 1960s

Auckland’s longest-serving mayor, Sir Dove-Myer Robinson, pushed for an underground rail loop known as Robbie’s Rapid Rail, including connections to Whangaparāoa, Hobsonville, Howick, the airport and an underground CBD rail loop.

1975

Robbie’s Rapid Rail was scuppered by the newly elected National government led by Muldoon.

2014

AT suggested light rail from CBD to Mt Roskill with main roads into the city reaching near capacity.

Mayor Len Brown wanted the focus to stay on getting government approval for the City Rail Link.

2016

During his by-election campaign in Mt Roskill, Michael Wood promised to fast-track a light rail system from Auckland’s Wynyard quarter to Mt Roskill.

2017

During the election campaign, Labour pledged it would build light rail from downtown Auckland to the airport within a decade.

June 2020

Then-Transport Minister Phil Twyford announced Cabinet had agreed to suspend the project until after the election because Government parties were unable to reach an agreement, with the Greens in favour but NZ First refusing to support it.

March 2021

Transport Minister Michael Wood sent light rail back to the drawing board, tasking a group of experts to develop a business case to revive the project.

https://www.timmccready.nz/wp-content/uploads/2021/12/Infrastructure-light-rail-Auckland-Dec21.jpg7831054tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2021-12-01 12:39:012021-12-02 12:44:40Infrastructure: Auckland’s light rail project poised to take a major step (NZ Herald)

Green finance is an important focus for ICBC. Kevin Xu explains to Tim McCready how the bank is active in global sustainable financial governance, learning from international practical experience, and contributing financial power to serve the sustainable development of the economy, society and environment.

Herald: ICBC’s attention to environmental, social, and governance (ESG) factors is growing. How is this affecting the bank’s involvement in international infrastructure projects?

Kevin Xu: ICBC has fully integrated ESG and green financial management into its investment and financing processes. Our head office has formulated green investment and financing policies for 16 sectors and nearly 50 industries, including infrastructure construction, and has positioned key areas such as green transportation, clean energy, energy conservation and environmental protection as active or moderate entry into the industry.

Environmental, climate and social risks arising from the credit granting process have been brought under classified management. Differentiated credit policies have been implemented in domains such as economic capital occupation, authorisation, pricing, scale, and a “one-vote veto system” is used for environmental protection. Green management requirements are extended to a wide range of investment and financing businesses lines such as bonds, wealth management, leasing.

ICBC New Zealand follows head office’s approach and has been actively involved in local infrastructure projects. More than NZ$300 million in loan commitments has been provided to support NZ renewable energy, sustainable projects in the past 12 months.

Herald: What factors do you take into account when integrating ESG factors into investment decisions?

Xu: We pay close attention to hazards and related risks that financing customers and related parties may bring to the environment and society in construction, production, and business activities. This includes energy consumption, pollution, land, health, safety, resettlement, ecological protection, environmental and social issues related to climate change.

ICBC implemented the “one-vote veto for environmental protection”for the entire investment and financing business process. The customer credit risk rating has embedded ESG factors.

Environmental risk factors are included in the customer rating model, including corporate environmental credit rating and green credit classification index. For corporates that are environmentally unqualified or unfriendly, the rating model will prescribe a limit to the customer’s credit rating.

The customer rating model covers governance risk factors, and incorporates corporate governance and corporate management indicators, including corporate governance structure, shareholder control, and related party transactions.

The inclusion of negative environmental events in the rating and early warning monitoring system, including factors such as environmental violations.

Our head office also clearly requires relationship managers to prudently evaluate the environmental and social risks of customers during the due diligence process and has introduced relevant supporting policies and systems.

Herald: What else does the bank take into consideration for infrastructure projects?

Xu: We also consider credit risks, market risks, country risks and other related factors that may affect investment safety and returns.

ICBC implements a unified credit risk appetite for all types of credit risk exposures across the bank, and implements full-process management of credit risk, covering the entire process from customer investigation, credit rating, loan evaluation, loan review and approval, loan issuance to post-loan monitoring.

For cross-border investment and financing, we also need to pay attention to the country risk of the country or region where the counterparty is located. ICBC uses a series of management tools to manage and control country risk, including country risk assessment and ratings, country risk limits, country risk exposure statistics and monitoring, and stress testing, etc.

Anti-Money Laundering is also the focus of our attention in handling investment and financing business. We strictly abide by relevant Anti-Money Laundering laws and regulations and steadily promote customer identification governance and high-risk areas management.

Herald: What impact has the pandemic had on ICBC’s infrastructure projects?

Xu: The outbreak of the pandemic and its prolonged duration have had varying degrees of impact on many industries, including infrastructure, and some projects are facing a certain degree of difficulties in supply chain operation and capital turnover.

ICBC actively fulfils its responsibilities as a corporate citizen by coordinating the prevention and control of the pandemic, financial security, and operation and management, and actively carrying out special activities to ensure the sustainability of the supply chain of large enterprises and the uninterrupted capital chain of small and medium-sized enterprises.

In the global fight against the pandemic, we will fulfil our responsibility, demonstrate our care and concern, and protect our beautiful home together.

Yangjiang Nanpeng offshore wind farm

ICBC approved a loan of RMB 1.6 billion yuan for the Yangjiang Nanpeng Island offshore wind farm project.

The 401.5MW project features 73 wind turbines and is the first single large capacity offshore wind power project in China. It is also the first offshore wind power project in Guangdong Province that is more than 10 kilometres away from the coastline and more than 10 metres deep.

Completed at the end of last year, the offshore wind farm can generate 1.015 billion kWh of annual on-grid power. This is expected to save 311,500 tons of standard coal and reduce carbon dioxide emissions by 828,800 tons every year.

Dubai solar thermal power plant

ICBC is the lead arranger for the construction of one of the world’s largest and most advanced solar thermal power plants.

The 700MW concentrated solar power and 250MW solar photovoltaic power station in Dubai has been jointly invested by Dubai Electricity and Water Authority (DEWA), ACWA and Silk Road Fund.

With a total investment of US$4.3 billion, the project is the largest new energy project financing in the world and has been highly recognised by the market. As the lead bank, ICBC arranged a US$2.5b senior syndicated loan with members from China, Europe and the UAE.

Concentrated power systems generate solar power by focusing a large area of sunlight into a small area.

The light is converted to heat, which is stored in molten salt to supply electricity on demand during the day and through the night.

This method of power generation makes up for the instability of solar power generation and the impact on power grids and ensure the stability of power supply.

The power plant is an important project under Dubai’s clean energy strategy and is expected to provide clean power to more than 270,000 households in Dubai every year, with zero emissions of carbon and pollutants.

The power plant will reduce carbon dioxide emissions by 1.6 million tons and will create 4000 direct jobs and more than 10,000 indirect jobs, providing local employment and economic development.

Baodi district solid waste power generation

With the increasing volume of municipal solid waste in Baodi District, Tianjin, China, the capacity of the original landfill site was not able to meet the needs of the community. To solve this problem, Tianjin Quantai Domestic Waste Treatment launched a domestic waste incineration power generation project.

ICBC granted a loan of RMB255 million yuan to assist with construction. The project began operations in December 2020 and has changed the method of domestic waste treatment from landfill to incineration. It is preventing the pollution of domestic waste into the soil and underground water sources and reducing reliance on fossil fuel-based power and heat sources and CO2 emissions by using waste as a resource for power generation.

• Kevin Xu is Team Head, Corporate & Institutional Banking at ICBC New Zealand.

ICBC is a sponsor of the Herald’s Infrastructure report.

https://www.timmccready.nz/wp-content/uploads/2021/12/Infrastructure-Green-credentials-ESG-Dec21.jpg730496tim.mccreadyhttps://www.timmccready.nz/wp-content/uploads/2024/03/TimMcCready_banner.pngtim.mccready2021-12-01 09:36:322021-12-02 12:44:49Infrastructure: Credit for green credentials (NZ Herald)

The full APEC CEO Summit is now available to watch, free, here.

Over two days in November, the world’s most influential political, business and thought leaders came together for the APEC CEO Summit 2021 to discuss ways the region can learn from each other and work together and to ensure it emerges from the pandemic stronger than ever.

The Summit addressed challenges and opportunities presented by the current situation, with a focus on five themes: the state of the world with, and post Covid; the digital disruption opportunity; the primacy of trust; the future of energy; and the sustainability imperative.

The state of the world with and post-COVID

The Summit was set at a complicated economic period as the world rebuilds in the wake of the pandemic. Just a year prior, the region’s economy saw a record contraction of -5 per cent, with estimates suggesting the Asia-Pacific lost over $2 trillion in potential trade over 2020.

This downturn was both faster and deeper compared to the global financial crisis – although will likely be shorter. Demonstrating this rapid turnaround, the last quarter saw record growth of 10 per cent in the region.

Keynotes from PwC global chair Bob Moritz and OECD Secretary-General Mathias Cormann, along with Dr Alan Bollard’s panel discussion on the economic state of the world helped to decipher the recovery and set the scene for the Summit. While the tone from speakers was optimistic, they cautioned the economy is still significantly impacted by the ongoing disruption of the pandemic and can be seen reflected in myriad contradictions.

The dramatic increase in trade is predominantly occurring in merchandise, with the region experiencing a chronic shortage of goods to meet demand, yet services trade is still worryingly negative.

Domestic investment has been increasing, but foreign direct investment is at a 20-year low.

Costs and wages are increasing, but productivity is stagnant.

Jobs are being displaced, but skills shortages are being reported widely across the region.

Uncertainty and significant downside risks remain, including inflationary pressures and the emergence of new Covid strains, vaccination levels and continued disruption from the pandemic – including the fourth wave beginning to sweep through Europe.

But the recovery is also providing the region tremendous opportunity – particularly for those businesses able to adapt and grow quickly and create supply chains that are robust and scalable.

Prime Minister Jacinda Ardern, this year’s APEC chair, said in her opening address:

“We have a saying in New Zealand. He rau ringa e oti ai – many hands make light work.

“The heavy load of a global pandemic that in equal measure threatens lives and livelihoods has been countered only with an extraordinary commitment to unity, partnership and progress in spite of the challenges.”

Former New Zealand Prime Minister and Administrator of United Nations Development Programme Helen Clark shared a similar sentiment, reminding delegates that they must work together and grab hold of the positives that can come from standing up to a crisis.

“We can strengthen our national systems for pandemic preparedness and response, and we can strengthen the global systems. All of that is good for business,” she said.

“If we are looking at the world we are trying to create, inclusion going forward is critical. But we must also build in resilience. Because if we don’t have resilient systems like with pandemic preparedness and response, we will repeat these lessons over and over.”

Recently elected President of Peru, José Pedro Castillo Terrones, shared a similar view, noting the APEC forum “is an important space for coordinating measures and identifying good public policy practices to face complex health and economic challenges.”

The digital disruption opportunity

While all economies across the APEC region have been impacted by the pandemic, there is clear evidence that those with digital readiness endured the pandemic and rebounded better.

Economies with both physical and digital infrastructure have been faster to deploy digital tools in the fight against Covid-19 – including contact tracing, proof of vaccine and digital trade facilitation – which has enabled them to keep their economies more open.

The pandemic acted as an accelerant and removed hurdles for innovation. Five years’ worth of technology adoption occurred within the first eight weeks of the pandemic, and the importance of its role as an enabler of trade was reiterated in almost every session at the Summit.

“The companies without digitalisation have been hit harder,” said Diane Wang, chair and CEO of DHGate. “They are at a crossroads… the choices we make today will have consequences on gender equality, digital equality and inclusive growth, for decades to come.”

In her keynote address, technology entrepreneur Amber Mac cautioned CEOs that “it may feel like there is a thick line between what you do and what big tech does, but as you embrace a tech-first strategy – an obvious path to succeed in today’s digital world – that line will soon begin to blur.”

Companies, government, and the public sector were urged to continue to seize the opportunities from digitalisation, with a heavy emphasis that the economic recovery post-Covid will continue to be digitally enabled.

Micro, small and medium enterprises (MSMEs) are particularly vulnerable to the economic impacts of the pandemic. With MSMEs making up over 97 per cent of all enterprises in the region and employing over half the workforce, digital adoption and access to innovation and will be essential for all business.

This was highlighted by Singapore Prime Minister Lee Hsien Loong, who stressed that most SMEs are not as digitally prepared as large businesses, and risk being left behind. “APEC economies must help SMEs and their workers make the digital transition,” he said.

He also acknowledged that the rapid uptake of digital innovation means that APEC economies need to do more to invest in the digital frameworks of the future, including digital identity, digital payments solutions, data exchange, data authorisation and consent.

Australian Prime Minister Scott Morrison used his address to express his concern over the rise of technology, and the ability for it to be used for bad, as well as good.

Morrison called for stronger rules for the tech sector and suggested it would be better for the sector to work in partnership with governments on regulation – saying that if not, governments will do it anyway, and “will stuff it up because they don’t understand it the same way.”

The primacy of trust

Along with digital adoption, the pandemic has also accelerated the erosion of trust around the world. There is an epidemic of misinformation and widespread mistrust of societal institutions and leaders around the world.

This extends to business, and as trust expert and public relations leader Richard Edelman told the Summit, earning trust has never been more important – or more challenging.

He described how employees have emerged as the most important stakeholder in business, with people “voting with their feet” and making major decisions – including what they buy and who they work for – based on personal beliefs.

The growing expectation of business to focus on societal engagement with the same rigor, thoughtfulness and energy used to deliver on profit was evident from delegates – the primacy of trust quickly became the most interactive session at the Summit, attracting robust discussion through the conference platform.

Edelman explained how consumers, employees and other broad stakeholders are paying more attention to what businesses say and do, and how they respond to issues including climate change, racial injustice, and other societal issues.

Intrinsically tied into trust is the need for business to apply environmental, social and governance (ESG) principles to their strategy and operations to create value for all of society.

Reiterating Edelman, the ESG panel told the Summit that there is now a much broader group of stakeholders that must be considered, including employees and the community. But beyond this, there is a growing consensus that ESG has become an extremely powerful driver for business success and financial return and is no longer seen as something that only adds costs to business.

The panel called for business leaders across the region to put ESG front and centre, integrating the principles into the purpose and values of an organisation and ensuring their commitment is actionable, verifiable, and transparent.

“The actions required are expensive, substantial, and they have to be core to an organisations strategy,” said McKinsey’s Andrew Grant. “They can’t just be window dressing or a box-ticking exercise.”

The panel said that businesses must lean in and recognise that doing good for society is also good for business.

This call for business to be a force for good in the world was repeated in the highly anticipated keynote address from international human rights lawyer Amal Clooney. She told delegates that we no longer live in a world where businesses can say ‘human rights are none of our business’.

“It is increasingly difficult for companies to say ‘we are just here to make a profit’ and bury their heads in the sand,” she said.

“Businesses, big multinational corporations, and tech companies in particular are a key part of our multilateral world of decision-makers, and each one will decide whether to be a force for good or complicit in abuses of power.”

The sustainability imperative